The Fed hiked its benchmark Fed Funds Rate despite signs of cooling inflation and concerns about the banking sector. Plus, job growth isn’t as strong as it seems while home prices have reached an inflection point. Here are the key stories:

- Fed Hikes Rates Another 25 Basis Points

- Strong Jobs Report or Not Really?

- What's Really Boosting Private Payrolls?

- Challenges Remain for Job Seekers

- Appreciation Data Turning Around

Fed Hikes Rates Another 25 Basis Points

The Fed hiked their benchmark Fed Funds Rate by 25 basis points at their meeting last Wednesday, bringing it to a range of 5% to 5.25%. The Fed Funds Rate is the interest rate for overnight borrowing for banks and it is not the same as mortgage rates. When the Fed hikes the Fed Funds Rate, they are trying to slow the economy and curb inflation. This was the Fed’s tenth hike since March of last year.

What’s the bottom line? The Fed’s decision to hike the Fed Funds Rate was unanimous, despite clear signs of falling inflation, forecasts of a recession, and concerns about the banking sector.

And while Fed Chair Jerome Powell stressed that the banking system is “sound and resilient,” one result of the Fed’s rate hikes is the stress they have put on many regional banks. Depositors have been incented to withdraw their money and invest it in higher-yielding money market accounts or short-term treasuries. Over the last two months, three banks with a combined $550 billion in assets have failed, which is 50% more than the 511 banks that have failed since 2009. The stability of regional banks is crucial, as they make up almost 40% of all loans.

There was a big change to the Fed’s policy statement, which saw the removal of language saying they “anticipate” further rate hikes would be needed. Instead, the Fed said that going forward they would determine whether additional firming policy would be appropriate. This lays the groundwork for a pause in rate hikes at their next meeting in June, although Powell noted in his press conference that the Fed has not made that decision as of yet. He also denied the Fed would cut rates this year even though economists forecast otherwise.

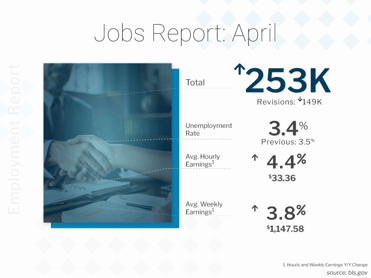

Strong Jobs Report or Not Really?

The Bureau of Labor Statistics (BLS) reported that there were 253,000 jobs created in April, which was much larger than estimates. However, substantive revisions to the data from February and March subtracted 149,000 jobs in those months combined, which tempered April’s gains. The unemployment rate fell from 3.5% to 3.4%.

What’s the bottom line? There are two reports within the Jobs Report and there is a fundamental difference between them. The Business Survey is where the headline job number comes from, and it's based predominately on modeling and estimations. The Household Survey, where the Unemployment Rate comes from, is derived by calling households to see if they are employed.

The Household Survey has its own job creation component, and it showed some underlying weakness with only 139,000 new jobs created last month. Plus, the labor force decreased by 43,000, which is not a positive sign. When we combine these two factors, the unemployment rate did decline – but not because of strong job growth.

In addition, while the headline job growth number appeared strong, there were some cracks in the data. One of the biggest reasons we saw job gains was the birth/death model, where the BLS estimates hiring from new business creation relative to closed businesses. The problem with this modeling is it overestimates during the inflection point of a downturn (like we’re in right now) and underestimates at the inflection of an upturn after a recession.

In April, this modeling added 378,000 jobs but it’s hard to believe that many businesses were created last month in the current economic climate where there is less lending from banks.

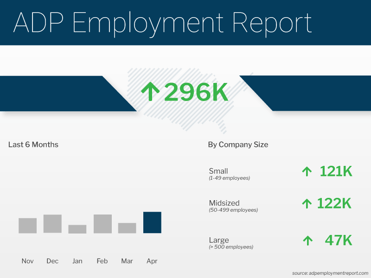

What's Really Boosting Private Payrolls?

Private payrolls nearly doubled expectations last month, as the ADP Employment Report showed that there were 296,000 jobs created in April. Annual pay for job stayers increased 6.7% and job changers saw an average increase of 13.2%. While these figures are still high, they reflect a year-long slowdown and lower wage-pressured inflation, with job-changers in particular seeing the slowest pace of pay growth since November 2021.

What’s the bottom line? The leisure and hospitality sector once again led the way with 154,000 job gains, and this sector has been a huge driver of job growth after the massive losses seen during the height of the pandemic. However, these jobs may not bolster the overall private payroll total for much longer. In April 2019, there were 16.2 million leisure and hospitality employees and there are now 16.25 million after last month’s gains, meaning we have eclipsed where we were pre-Covid.

In addition, private sector job growth has been quite volatile so far this year, with monthly gains averaging 205,000 from January through April. This is compared to an average of 306,000 new jobs per month throughout last year, so we’re seeing a clear slowdown notwithstanding April’s strong print.

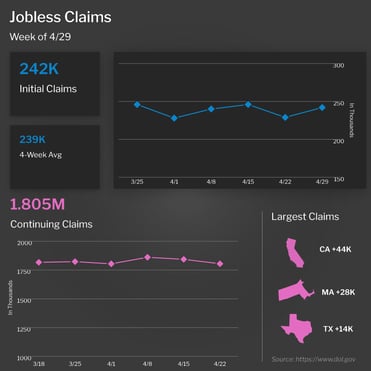

Challenges Remain for Job Seekers

The number of people filing for unemployment benefits for the first time rose by 13,000 in the latest week, as 242,000 Initial Jobless Claims were reported. Continuing Claims, which reflect people continuing to receive unemployment benefits after their initial claim is filed, declined by 38,000 to 1.805 million.

What’s the bottom line? Jobless Claims can be volatile from week to week, but they continue to trend higher. Initial Jobless Claims have remained above 200,000 since early February. Plus, the four-week average of Initial Jobless Claims, which smooths out some of the weekly fluctuation among first-time filers, has hovered around 240,000 near a yearly high in recent weeks. Meanwhile, Continuing Claims have now risen by over 500,000 since the low reached last September, which shows the challenges people are subsequently facing as they search for new employment.

Housing Market at a Turning Point

CoreLogic’s Home Price Index showed that home prices nationwide rose by 1.6% from February to March and they were 3.1% higher when compared to March of last year. This follows February’s 0.8% rise in home prices, suggesting that the housing market is at a turning point. CoreLogic forecasts that home prices will rise 0.8% in April and 4.6% in the year going forward, which is an upward revision from 3.7% in February’s report.

In addition, other prominent appreciation reports have shown that home prices are on the rise again, including those by Case Shiller (+0.2% in February), the Federal Housing Finance Agency (+0.5% in February), Black Knight (+0.5% in March) and Zillow (+0.9% in March). This is further evidence that home prices have reached an inflection point.

What’s the bottom line? CoreLogic’s Chief Economist Selma Hepp said, "While housing markets across the country continue to send mixed signals, prices in many large metros appeared to have turned the corner, with the U.S. recording a second month of consecutive monthly gains. At 1.6%, the month-over-month increase was twice the average seen between 2015 and 2020.”

She added that, “The monthly rebound in home prices underscores the lack of inventory in this housing cycle. In addition, while the lack of affordability generally weighs on home price growth, mobility resulting from remote working conditions appears to be a current driver of home prices in some areas of the country."