Uncertainty surrounding the debt ceiling caused volatility in the markets, while inflation was hotter than expected in April. Tight supply continues to be a key factor impacting home sales. Here are the headlines.

- Better Progress to Come on Inflation

- “Sizeable Increase” Needed in Housing Inventory

- New Home Sales Hit 13-Month High

- Unemployment Claims Reflect Challenges for Job Searchers

- First Quarter GDP Revised Higher but Still Disappointing

Better Progress to Come on Inflation

The Fed’s favorite measure of inflation, Personal Consumption Expenditures (PCE), showed that headline inflation increased 0.4% in April, while the year-over-year reading ticked higher from 4.2% to 4.4%. Core PCE, which strips out volatile food and energy prices, also rose by 0.4% with the year-over-year change up from 4.6% to 4.7%. All these readings were hotter than expected, as energy prices and used cars pressured inflation higher.

What’s the bottom line? Inflation is the arch enemy of fixed investments like Mortgage Bonds because it erodes the buying power of a Bond's fixed rate of return. If inflation is rising, investors demand a rate of return to combat the faster pace of erosion due to inflation, causing interest rates to rise like we saw throughout much of last year.

While inflation moved in the wrong direction in April, the coming months will likely see nice progress made toward lowering inflation. This is because inflation is calculated on a rolling 12-month basis, so the total of the past 12 monthly inflation readings gives us the year-over-year rate of inflation. Headline inflation last year was 0.6% in May and 1% in June, so if we continued to see 0.4% readings over the next two reports, year-over-year inflation would drop from 4.4% to 3.6%.

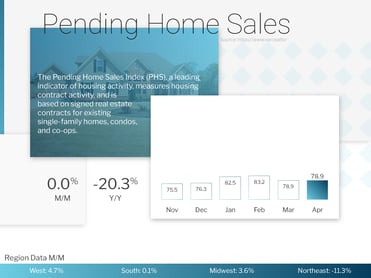

“Sizeable Increase” Needed in Housing Inventory

Pending Home Sales remained at the same level from March to April, which was a bit below estimates looking for a 1% gain. While the West, Midwest and South all saw increases, there was a big decrease in the Northeast which pulled the index down overall. Sales were also 20.3% below the amount recorded in April of last year, though this was an improvement from the annual difference of -23% reported for March.

Pending Home Sales are a crucial measure for taking the pulse of the housing market. The data is considered a forward-looking indicator of home sales because it measures signed contracts on existing homes, which represent around 90% of the market.

What’s the bottom line? Tight supply of existing homes remains the key hindrance to signed contracts this spring. Lawrence Yun, chief economist for the National Association of REALTORS®, explained, “Not all buying interests are being completed due to limited inventory. Affordability challenges certainly remain and continue to hold back contract signings, but a sizeable increase in housing inventory will be critical to get more Americans moving."

New Home Sales Hit 13-Month High

-png.png?width=371&height=247&name=New-Homes-Sales-v2%20(1)-png.png)

New Home Sales, which measure signed contracts on new homes, rose 4.1% from March to April to a 683,000-unit annualized pace. Sales are at their best level in thirteen months, and they were also 11.8% higher than in April of last year.

The median sales price fell from $455,800 in March to $420,800 in April. Note that this figure is not the same as appreciation but represents the mid-price and can be skewed by the mix of sales among lower-priced and higher-priced homes. Recent appreciation reports from Case-Shiller, CoreLogic and the Federal Housing Finance Agency have shown that home prices are rising again.

What’s the bottom line? The rise in signed contracts for new homes correlates with the low level of existing homes that are listed for sale. This has helped boost confidence among homebuilders, which is a positive sign as more new homes are needed to meet the overall demand among buyers. While there were 433,000 new homes for sale at the end of April, only 70,000 were completed, with the rest either not started or under construction.

This disparity between the high demand for homes and tight supply of both existing and new homes will continue to be supportive of home prices, providing opportunities for buyers who are ready to start taking advantage of appreciation gains.

Unemployment Claims Reflect Challenges for Job Searchers

-png-May-26-2023-12-05-49-0163-PM.png?width=371&height=371&name=jobless-claims%20(2)-png-May-26-2023-12-05-49-0163-PM.png)

Initial Jobless Claims rose by 4,000 in the latest week, as 229,000 people filed for unemployment benefits for the first time. However, there was a negative revision to the previous week’s data subtracting 17,000 claims, so the net number over the past two weeks is lower. While this sounds like positive news on the surface, part of the decline stems from fraud that was discovered in both Massachusetts and Kentucky, which had spiked the number of filings.

Continuing Jobless Claims declined by 5,000 in the latest week though they remain elevated at 1.794 million, which is well above the low of 1.289 million seen last September. This upward trend shows the difficulties many people are having as they search for new employment.

First Quarter GDP Revised Higher but Still Disappointing

The second reading of first quarter 2023 Gross Domestic Product (GDP) showed that the U.S. economy grew by 1.3%. While this was an improvement from the initial estimate of 1.1%, it is still significantly lower than the 2.6% growth reported in the fourth quarter of last year. Note that this data is subject to further revision when the final report is released on June 29. However, given that GDP functions as a scorecard for the country’s economic health, the disappointing reading is a further sign that the economy slowed faster than expected in the first three months of this year.