Inflation continues to march lower while tight housing supply and elevated mortgage rates remain key influences on home sales and home prices. Here are last week’s stories:

- Inflation Makes Progress Lower

- Pending Home Sales Tumble in August

- New Home Sales Hit Slowest Pace Since March

- Record High for Home Prices

- Initial Unemployment Claims Remain Tame

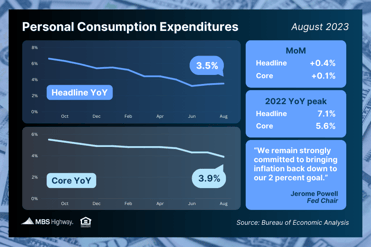

Inflation Makes Progress Lower

August’s Personal Consumption Expenditures (PCE) showed that headline inflation increased by a lower-than-expected 0.4%. The year-over-year reading rose from 3.4% to 3.5%, though the increase was due to revisions in prior reporting. Core PCE, the Fed’s preferred method which strips out volatile food and energy prices, rose by 0.1% in August with the year-over-year reading falling from 4.3% to 3.9% – the lowest level in two years.

What’s the bottom line? The Fed has hiked its benchmark Fed Funds Rate (the overnight borrowing rate for banks) eleven times since March of last year to try to slow the economy and curb inflation. While inflation is still elevated, it has made a big improvement from the 7.1% peak seen last year and is now less than half that amount at 3.5% on the headline reading.

Plus, if we annualize the last six months’ worth of Core PCE readings (which the Fed did during their last meeting), Core PCE would equal 2.9%. This is a large drop from 3.4% in the previous report and not far above their 2% target. Will this progress be enough for the Fed to pause further rate hikes? We’ll find out at their next meeting on November 1.

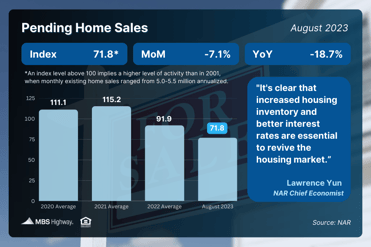

Pending Home Sales Tumble in August

Pending Home Sales fell 7.1% from July to August, with sales also 18.7% below the level seen a year earlier. This data measures signed contracts on existing homes, making it a forward-looking indicator for closings as measured by Existing Home Sales. August’s level of signed contracts suggests that closings in September will likely come in at an annualized pace under 4 million.

What’s the bottom line? Some would-be homebuyers have pressed pause on their purchase due to high rates and low inventory. Lawrence Yun, chief economist for the National Association of REALTORS® (NAR), explained, "It's clear that increased housing inventory and better interest rates are essential to revive the housing market.”

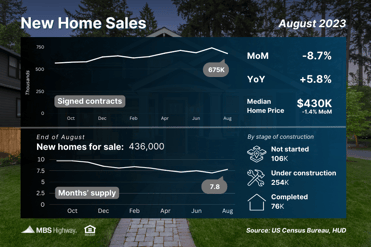

New Home Sales Hit Slowest Pace Since March

New Home Sales, which measure signed contracts on new homes, fell 8.7% from July to August to a 675,000-unit annualized pace. However, there was a positive revision to the number of signed contracts in July, and sales are still higher than they were a year earlier.

What’s the bottom line? Buyers continue to turn to the new construction market due to the lack of existing homes for sale. However, more “available” supply of new homes is needed to meet demand. Of the 436,000 new homes available for sale at the end of August, only 76,000 were completed, with 254,000 under construction and 106,000 not even started yet.

The tight supply of both existing and new homes will continue to be supportive of home prices. On that note, the median sales price for new homes was $430,300, which was down from $440,300 a year ago. While this may sound like home prices are declining, this figure is not the same as appreciation but represents the mid-price and can be skewed by the mix of sales among lower-priced and higher-priced homes.

Multiple appreciation reports have reported record high home price growth in their respective indexes, as detailed below.

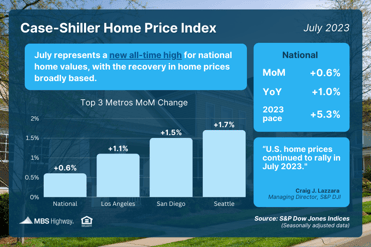

Record High for Home Prices

The Case-Shiller Home Price Index, which is considered the “gold standard” for appreciation, showed home prices nationwide rose 0.6% from June to July after seasonal adjustment, marking the sixth consecutive month of gains. The Federal Housing Finance Agency’s (FHFA) House Price Index also saw home prices rise 0.8% in July, with their index reporting gains every month so far this year.

Note that FHFA’s report measures home price appreciation on single-family homes with conforming loan amounts, which means it most likely represents lower-priced homes. FHFA also does not include cash buyers or jumbo loans, and these factors account for some of the differences in the two reports.

What’s the bottom line? Home values have hit new all-time highs according to Case-Shiller, FHFA, CoreLogic, Black Knight and Zillow, more than recovering from the downturn we saw in the second half of 2022. This year, prices are on pace to appreciate between 5-9% depending on the index, based on the reported pace of appreciation through July. These indexes show that now remains a great opportunity for building wealth through homeownership and appreciation gains.

Initial Unemployment Claims Remain Tame

Initial Jobless Claims rose by 2,000 in the latest week, just above the previous week’s eight-month low, with 204,000 people filing for unemployment benefits for the first time. The low level of first-time filings suggests that employers continue to hold on to workers.

Continuing Claims also rose by 12,000, with 1.67 million people still receiving benefits after filing their initial claim. This data has been trending lower since topping 1.861 million in early April, reflecting a mix of people finding new jobs and benefits expiring.

What’s the bottom line? The Fed has been looking for clear signs that the labor market is softening as they consider further rate hikes this fall. Upcoming labor sector data will also play a pivotal role in the Fed’s next rate decision, which will be announced on November 1.